2024 is turning out to be a solid year for the global semiconductor industry, driven by multiple catalysts. These include the booming demand for chips that can manage artificial intelligence (AI) workloads, a turnaround in the smartphone market’s fortunes, and a recovery in the personal computer (PC) market.

These factors explain why the global semiconductor industry’s revenue is expected to jump 16% in 2024 to $611.2 billion, according to World Semiconductor Trade Statistics (WSTS). That points toward a nice turnaround from last year, when the semiconductor industry’s revenue fell 8%. Even better, the semiconductor space is expected to keep growing in 2025 as well, with WSTS projecting a 12.5% increase in the industry’s earnings to $687.4 billion next year.

More specifically, WSTS predicts a whopping 25% increase in the memory market’s revenue in 2025 to $204.3 billion. As it turns out, memory is expected to be the fastest-growing semiconductor segment next year as well, following an estimated jump of almost 77% in this segment’s revenue in 2024.

There’s one company that could help investors tap this fast-growing niche of the semiconductor market next year: Micron Technology(NASDAQ: MU). Let’s look at the reasons why buying this semiconductor stock could turn out to be a smart move right now.

WSTS isn’t the only forecaster expecting the memory market to surge higher next year. Market research firm TrendForce estimates that the sales of dynamic random access memory (DRAM) could jump 51% in 2025, while the NAND flash storage market could clock 29% growth. Both these markets are expected to reach record highs next year.

The growth in these memory markets will be driven by a combination of strong demand and improved pricing. TrendForce is forecasting a 35% year-over-year increase in DRAM prices next year, driven by the increasing demand for high-bandwidth memory (HBM) that’s used in AI processors, as well as the growth in DRAM deployed in servers. Meanwhile, the growing demand for enterprise-class solid-state drives (SSDs) and the growth in smartphone storage will be tailwinds for the NAND flash market.

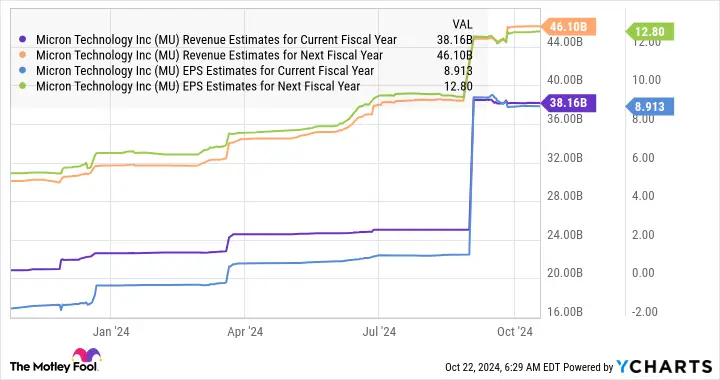

These positive trends explain why Micron is set to begin its new fiscal year on a bright note. The company’s revenue in fiscal 2024 (which ended on Aug. 29) increased 61% year over year to $25.1 billion. The company posted a non-GAAP (generally accepted accounting principles) profit of $1.30 per share, compared to a loss of $4.45 per share in fiscal 2023, driven by a big jump in its operating margin on account of recovering memory prices.

More importantly, Micron is expecting fiscal 2025 Q1 revenue of $8.7 billion at the midpoint of its guidance range. That would be a jump of 84% from the same quarter last year. The memory specialist has guided for non-GAAP earnings of $1.74 per share for the current quarter, up substantially from the loss of $0.95 per share it suffered in the same quarter last year.

The good part is that its top and bottom lines are expected to jump substantially in both fiscal 2025 and fiscal 2026 (see chart below).

MU Revenue Estimates for Current Fiscal Year Chart

It won’t be surprising to see Micron deliver such impressive growth thanks to the health of the memory market. However, there is a good chance it could end up exceeding analysts’ expectations.

Micron management remarked on the latest earnings conference call that it is “making investments to support artificial intelligence (AI)-driven demand, and our manufacturing network is well positioned to execute on these opportunities.” The company has guided for capital expenditures of $3.5 billion for the first quarter of fiscal 2025, which would be a big leap over the $1.7 billion capex it reported in the year-ago period.

Micron is doing the right thing by increasing its capex, as the company says that it has sold out its entire HBM production capacity for 2024 and 2025. The addressable opportunity in the HBM market is expected to grow from $4 billion in 2023 to $25 billion next year, per Micron’s estimates. So an increase in capital spending should allow Micron to shore up its production capacity and fulfill more demand, which could lead to a stronger-than-expected performance from the company.

Micron stock has been subject to some volatility this year, but it has still clocked respectable gains of 30%, as compared to the PHLX Semiconductor Sector index’s 25% jump. The stock, however, has gained impressive momentum since it reported its quarterly results on Sept. 25. There is a strong likelihood that it will be able to sustain this bull run in 2025 and beyond, thanks to the favorable dynamics in the memory market, as discussed.

We have already seen in the chart that Micron’s earnings could hit $8.91 per share in the current fiscal year before jumping to $12.80 per share in fiscal 2026. Assuming Micron does generate $12.80 per share in annual earnings after a couple of years and trades at 30 times forward earnings at that time, in line with the Nasdaq-100 index’s forward earnings multiple (using the index as a proxy for tech stocks), its stock price could hit $384.

That would be a big increase from Micron’s current stock price of around $109, suggesting that this chip stock could deliver outstanding gains over the next two years. Given that Micron is trading at just 12.5 times earnings right now, investors are getting a good deal on this tech stock that seems set to skyrocket going forward.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $20,803!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,654!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $404,086!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The "Aik News" platform provides the latest news about politics, business, sports, entertainment, and gadgets. We always strive to provide you with the latest information, so please subscribe to our newsletter.

Leave a Comment