After five years of closure, the Three Mile Island nuclear power plant is set to reopen. Known for the infamous 1979 partial meltdown that cemented its place in the annals of anti-nuclear activism, the plant is now being revived due to a shift in economic and energy trends.

At the core of the nuclear industry’s resurgence is the rising demand for electricity. The rapid expansion of power-hungry AI-driven data centers, combined with government initiatives promoting a transition from fossil fuels to electric power, has made it essential to boost electricity generation – and nuclear energy is once again becoming a key player in this landscape.

Watching the electric utility stocks for J.P. Morgan, analyst Jeremy Tonet writes of the sector’s growing shift toward nuclear, “We see structural tailwinds, including manufacturing onshoring, broader electrification trends (transportation, heating, and more), as well data center development underpinning a paradigm shift in power demand. We do not see competitive market supply growth matching this demand, enabling IPPs to capture outsized margins for an extended period of time,” Tonet explained. “More specifically, we see burgeoning hyperscaler demand growth focused on firm, carbon-free power, transforming nuclear power into a unique, scarce offering that will command a substantial premium.”

Following from this, Tonet goes on to recommend three nuclear power stocks for investors to buy – now, as the industry is beginning to power up. According to the data from TipRanks, these are all Buy-rated equities that have seen recent strong share appreciation – yet Tonet sees more upside ahead. Here are the details.

We’ll start with Talen Energy, a major independent power and infrastructure company on the North American scene. Talen was founded in 2015, and in its near-decade of business, which has already included bankruptcy in 2022 and restructuring the following year, has expanded to reach a market cap of $9 billion. The company focuses on delivering power generation that is both safe and reliable, providing investors with the most value for every megawatt of energy produced.

Talen’s power generation portfolio includes all of the major assets behind the U.S. electric grid: natural gas, coal, oil, and nuclear. The firm’s operations are built around its Susquehanna nuclear power plant, the nation’s sixth-largest operating nuclear power facility. Talen’s total portfolio has operations in five states—Maryland, Pennsylvania, New Jersey, Massachusetts, and Montana—and has a total of 10.7 gigawatts of power generation. Of that total, 2.2 gigawatts, or more than 20%, comes from the Susquehanna plant.

The Susquehanna operation delivers clean and reliable power, regardless of weather, 24 hours per day, 7 days per week, year-round—and its combination of reliability and high output has made Talen an important supplier for the data center industry, with a reputation for providing reliable power, on demand, to high-consumption customers.

These are the go-to requirements for AI and data center companies and help explain why Talen and Amazon, earlier this year, entered into a notable deal. In March, Amazon’s AWS spent $650 million to purchase Cumulus Data Assets, Talen’s data center campus. The 1,200-acre data center facility is adjacent to Talen’s Susquehanna plant, underscoring the close link between reliable power and the data center/AI/cloud computing segments.

Filling that power niche has brought financial rewards to Talen. In its last reported quarter, 2Q24, the company didn’t just generate electricity—it also generated profits. Talen reported an EPS of $7.60 in Q2, supported by revenues of $489 million. The top line was up more than 62% year-over-year and also fed into the year’s first-half free cash flow of $165 million. Even better for investors, TLN shares are up an impressive 178% year to date.

There are more gains on the way, according to JPM’s Tonet, who takes an upbeat stance on the firm. Tonet notes the AWS deal, as well as Talen’s potential for continued sales of clean electricity from Susquehanna, writing, “Talen’s first-of-a-kind TLN-AMZN deal presents a multi-decade opportunity for Susquehanna to sell premium, carbon-free power and meaningfully support the company earnings runway. Annual deal revenues could total $335-670mm in contracted annual revenue at the 480MW and 960MW scenarios, with some potential for pull forward of the high end… While we expect a broader policy debate over behind-the-meter arrangements and data center development to continue, given the macro demand for carbon-free power, we view TLN as well positioned to continue to convert Susquehanna’s remaining 1,748MW of capacity to premium contracted revenues.”

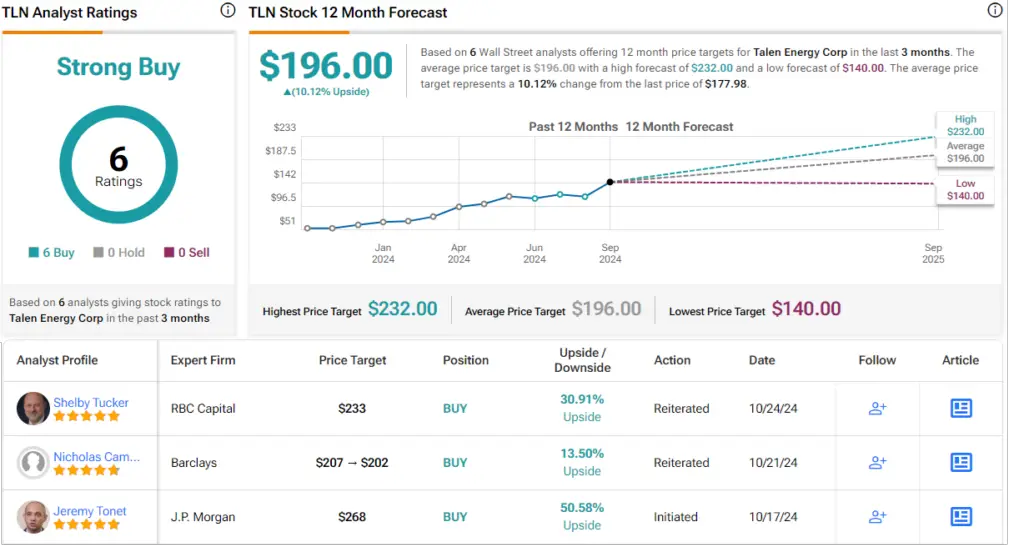

Tonet’s stance backs up his Overweight (i.e. Buy) rating on Talen, and his $268 price target points toward a 50.5% share appreciation on the one-year horizon. (To watch Tonet’s track record, click here)

Talen’s Strong Buy consensus rating is unanimous, based on six positive analyst reviews issued in recent months. The stock is selling for $177.98, and its $196 average target price suggests a one-year upside potential of 10%. (See TLN stock forecast)

Vistra Energy(VST)

Next on our list is Vistra Energy, a power company based out of Texas and providing utility-scaled electric power generation services. Vistra Energy is the US market’s largest competitive power generation company, and produces approximately 41,000 megawatts of electricity for more than 5 million customers. The company has over 6,800 people working its facility network. That network includes the full range of power generation plants – gas, coal, nuclear, and solar – as well as approximately 1,020 megawatts of battery power storage systems. Vistra is a major producer of zero-carbon power, and operates the nation’s second-largest fleet of nuclear power plants.

Vistra has been making moves to expand its nuclear power footprint. Back in March, the company completed its acquisition of Energy Harbor, adding 4 gigawatts of nuclear power generation to its portfolio and approximately 1 million customers to its rolls. And, in July, the company received a 20-year license from the Nuclear Regulatory Commission to continue operations of its Comanche Peak nuclear plant through the year 2053. This marks a 20-year extension of the original operating license.

This large-cap power company generated $3.85 billion at the top line in Q2 of this year, a figure that was almost 21% higher than the second quarter of last year – although it was $110 million below the forecast. The company reported net income of $467 million, while cash flow from operations came to almost $1.2 billion. Vistra has deep pockets, with $3.85 billion in available liquidity as of the end of Q2. That total included $1.62 billion in cash and cash equivalent assets.

We should note here that Vistra in September passed semiconductor chip maker Nvidia as this year’s biggest gainer among the S&P 500 stocks. VST shares are up 228% for the year-to-date, while Nvidia – no slouch – shows a 183.5% gain.

Analyst Tonet, in his report on Vistra, notes that the company’s chief asset is the sheer size of its power generation capacity. He writes, “Vistra stands out with an advantaged 41GW generation portfolio carrying leverage to base load power demand growth, with data center development, manufacturing reshoring, TX population growth, policy-driven coal retirements, and long-term electrification trends all together driving a potential ~40GW supply/demand gap by 2030 in ERCOT and a similar ~40GW gap in PJM.”

“With natural gas representing nearly 60% of VST’s fleet (or ~24GW), VST owns and operates more gas-fired generation than the next three publicly traded IPPs combined,” Tonet went on to add. “We view this gas-rich portfolio as uniquely positioned to benefit under a backdrop where base load power demand outpaces the supply of carbon-free resources and the time line to build new dispatchable plants. We anticipate environmental policies forcing significant coal plant retirements could further impact the supply-demand gap through the end of the decade.”

The JPM energy expert goes on to give VST an Overweight (i.e. Buy) rating, which he complements with a $178 price target. That target points toward a one-year gain of 42% in the coming year.

Like Talen above, Vistra has a unanimously positive Strong Buy consensus rating, based on 6 recent analyst reviews. (See VST stock forecast)

Constellation Energy Corporation (CEG)

Last on our list is Constellation Energy, the largest producer of clean energy in the US, generating as much as 10% of the nation’s carbon-free electrical power. Constellation has a total portfolio capable of generating 32,400 megawatts of power, based on nuclear, wind, solar, hydroelectric, and natural gas generation facilities. The company’s nuclear segment produces up to 19,000 megawatts of power – and includes the Unit 1 plant on Three Mile Island, which as noted above is set to reopen. Constellation is currently working on reconditioning the plant, with plans to reopen the facility in 2028 – and to sell the power to Microsoft, for the tech giant’s data center business.

News of the TMI Unit 1 restart, along with the prospective Microsoft deal, gave CEG shares a major boost. The stock jumped as much as 32% in September, and is up 127.5% for 2024 year-to-date.

As much as 90% of Constellation’s power generation is carbon-free, and the company aims to increase that percentage, in steps, to 100% by 2040. This is part of the company’s commitment to providing clean power – which it does, for more than 16 million homes.

On the financial side, Constellation has been consistently profitable for a while now, and generates high revenues. In its last report, covering 2Q24, the company showed a top line of $5.475 billion and a bottom-line non-GAAP EPS of $1.68. However, we should note that the revenues were mainly flat year-over-year and missed the forecast by $75 million, while the EPS was a penny below expectations.

Checking in one last time with JPM’s Tonet, we find the 5-star analyst bullish on CEG stock, basing his view on the company’s combination of scale and power capacity. Tonet writes, “Backed by nuclear PTCs offering a floor to power prices while retaining price upside and a scaled retail business, CEG carries industry-leading growth visibility through the end of the decade. The company targets a +13% base EPS CAGR through 2030, with even further upside potential from nuclear contracting and/or enhanced margins. We anticipate nuclear contracting to drive a large portion of CEG’s upside as the company secures long-term agreements with hyperscalers at premium prices, with opportunities landing on both sides of the meter, as demonstrated with the 835MW TMI restart. Alongside a comparatively strong balance sheet (<2.0x leverage) and IG ratings, CEG’s balanced all-of-the-above capital allocation also screens positively, with a mix of share repurchases, dividend growth, and growth projects, plus the potential for disciplined M&A.”

These comments support Tonet’s Overweight (i.e. Buy) rating, and his $342 price target indicates his confidence in a 29%-plus upside for the next 12 months.

Constellation’s 17 recent analyst reviews split 11 to 6 in favor of Buy over Hold, for a Moderate Buy consensus rating. With a trading price of $264.50 and an average target price of $277.53, CEG shares have a potential one-year upside of 5%. (See CEG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

The "Aik News" platform provides the latest news about politics, business, sports, entertainment, and gadgets. We always strive to provide you with the latest information, so please subscribe to our newsletter.

Leave a Comment