Bill Gross made a lot of money for his investors (and himself) at PIMCO, the investment management firm he co-founded. Forbes estimates his net worth at $1.7 billion. He made most of his money investing in bonds (he’s known as the “Bond King”).

Today, Gross favors a different type of income-generating investment: master limited partnerships (MLPs). Here’s a look at why he prefers them over other pipeline stocks for those seeking tax-advantaged income.

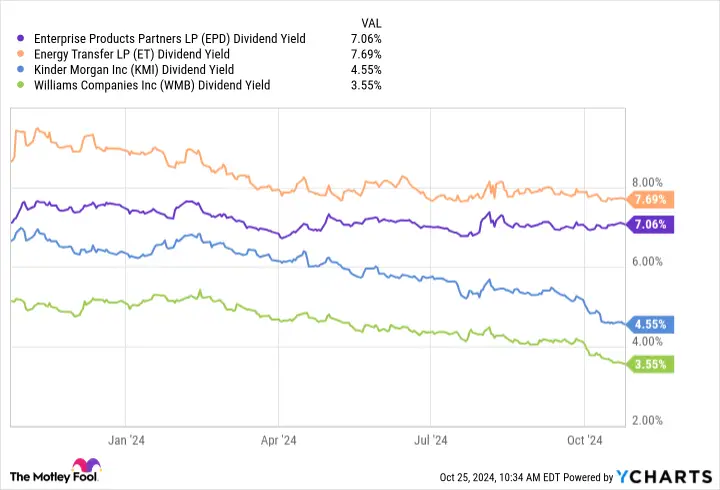

Bill Gross recently wrote about the benefits of investing in MLPs, like Enterprise Products Partners(NYSE: EPD) and Energy Transfer(NYSE: ET), over pipeline corporations, like Kinder Morgan (NYSE: KMI) and Williams(NYSE: WMB). For starters, the MLPs currently have much higher yields compared to their corporate peers:

All four energy midstream companies generate stable revenues backed by long-term contracts and government-regulated rate structures. Further, they all pay out around 50% of their predictable cash flow to investors in dividends (or distributions for the MLPs). The key difference between the two groups is their valuations.

Shares of Kinder Morgan and Williams have surged about 40% and 50%, respectively, this year, while units of the MLPs are up about 20%. Because of that, the pipeline companies now trade at about 20 times their earnings, while the MLPs sell for around 12 times their earnings.

In addition to earning a higher going-in income stream, MLPs offer a unique tax advantage. MLPs benefit from a tax-deferral feature on their distributions that can enable investors to defer taxes on a meaningful percentage of their distributions until they sell their units.

Gross did the math, writing: “The compounding deferral could add as much as 1% or so over a 5-10-year average holding period, turning the 8% average to a 9-10% dividend return on your portfolio.” That extra percentage point can add up over the long term.

Gross dove into the two main factors driving the disconnect between MLPs and pipeline stocks.He noted that many investors don’t like receiving the Schedule K-1 Federal Tax Forms MLPs send their investors each year (pipeline corporations send a 1099-DIV Form). Those K-1s can complicate and add to the expense of preparing individual taxes, so many investors avoid these entities.

Meanwhile, some pipeline companies have a competitive advantage in that they primarily transport natural gas (Kinder Morgan and Williams are leaders in gas infrastructure). That potentially positions them for more growth in the coming years as gas demand surges, fueled partly by the need to power data centers for artificial intelligence. That optimism over gas demand has driven up the valuations of Williams and Kinder Morgan this year.

However, MLPs have plenty of growth coming down the pipeline. Enterprise Products Partners has a multibillion-dollar backlog of commercially secured capital projects, providing growth visibility through 2026. Meanwhile, Energy Transfer has been consolidating the midstream sector and organically expanding its operations.

The MLPs are expanding their gas infrastructure and midstream footprints to support oil and refined products. In addition, they’re growing their export capacity. That growth should enable these MLPs to continue increasing their distributions. (Enterprise has raised its payment for 26 straight years, while Energy Transfer plans to grow its payout by 3% to 5% annually in the future.)

Add it all up, and MLPs trade at lower valuations and higher yields, offer better tax advantages and are still growing at a solid rate. That’s why Gross believes MLPs are a better long-term investment.

In addition to Energy Transfer and Enterprise Products Partners, he likes fellow MLPs Western Midstream, Plains All American Pipeline, MPLX, and Hess Midstream, which currently offer yields in the 7% to 9% range. While they all focus more on oil-related infrastructure, they expect to continue expanding their footprints and distribution payments in the coming years.

Bill Gross knows a thing or two about generating high returns from income-producing investments. While he became a billionaire by investing in bonds, he currently sees the best return potential from MLPs, thanks in part to their tax advantages. While MLPs have drawbacks, they offer attractive return potential, given their high-yielding distributions, which should grow in the coming years.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,154!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,777!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $406,992!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

Matt DiLallo has positions in Energy Transfer, Enterprise Products Partners, and Kinder Morgan. The Motley Fool has positions in and recommends Kinder Morgan. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

The "Aik News" platform provides the latest news about politics, business, sports, entertainment, and gadgets. We always strive to provide you with the latest information, so please subscribe to our newsletter.

Leave a Comment