The world is awash in semiconductors. Companies are spending tens of billions of dollars to build new computer chips for the artificial intelligence (AI) boom. It is no surprise, then, that one of the leading equipment makers for semiconductors, ASML (NASDAQ: ASML), was up 40% year to date at one point recently.

As of this writing, the company has given up all of these gains. Even though the narrative was for insatiable demand for semiconductors in 2024, ASML posted slowing orders in the third quarter due to struggles in every other segment outside of AI.

The stock is now down 36% from all-time highs set earlier this year, and yet it still trades at close to $700 a share, making it a potential stock-split candidate within the next few years.

Is it time to buy the dip on ASML with shares trading on the cheap?

Slowing orders, but demand for AI tools

ASML sells advanced lithography machines that semiconductor manufacturers use. With its cutting-edge technology, the company is the only one in the world that has extreme ultraviolet lithography (EUV) technology, making it the sole source for manufacturers looking to make the most advanced semiconductors. With no ASML machines, there would be no ultra-advanced AI chips from Nvidia.

The AI spending boom led investors to believe that orders for ASML would skyrocket, but that did not happen in the third quarter. Even though management said that spending for AI remains elevated, the Netherlands-based company only booked 2.6 billion euros ($2.8 billion) of orders committed to by customers in the period compared to more than 5 billion euros ($5.4 billion) of backlog a year ago.

Revenue (not backlog) grew to around $8.1 billion in the third quarter. ASML has a sizable backlog, so any orders placed today won’t be converted into revenue for at least a year, if not longer. But it can be a good barometer for what revenue growth could look like over the next few years.

In 2024, ASML is now guiding for $38.4 billion in revenue. In 2025, it expects between $32.5 billion and $38 billion, which is at the lower end of its previous long-term projection. Given this downgrade in guidance, it is no surprise that the stock plummeted after the recent earnings report.

Focus on long-term projections

The semiconductor equipment market is cyclical. ASML is going through a down cycle right now in every other segment besides AI. This is why orders are low and projections for 2025 revenue growth have come down.

This doesn’t mean the semiconductor market is done growing over the long term. Through 2030, ASML expects spending to rise by an average of 9% per year. With this increase in sales, the company should grow revenue at a double-digit rate through the end of the decade.

If revenue grows 10% annually to 2030, the company will be generating around $54.2 billion in sales a year by 2030.

What will that equate to in profits? In the last few years, ASML has maintained an operating margin of around 30%, which I think it can maintain in the future. This would mean $16.3 billion in operating earnings in 2030, a multiple of 17 versus its current market cap of $271 billion.

For such a high-quality company, this looks cheap but is not an extreme bargain. I think the stock will do well over the next five years if these projections are met.

Buy it for dividend growth?

ASML’s stock can appreciate over the next five years for patient shareholders. And unlike other hypergrowth and cutting-edge technology companies, it can also provide dividend payments to fuel total returns.

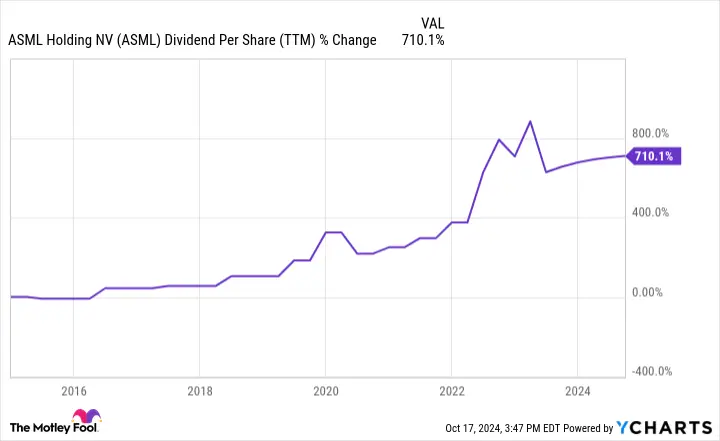

The stock’s dividend has grown by 710% in the last 10 years. The current yield is quite low at below 1%, but there is a lot of room to expand if the dividend keeps growing. Management said it wants to grow the dividend and keep repurchasing stock, which will help raise the payout. ASML’s shares outstanding have fallen by around 10% in the last 10 years.

With the dividend income and the chance for more price appreciation, ASML looks like a fine stock to buy at these prices. And with its price approaching $1,000 a share, it is a likely candidate for a stock split in the next few years.

Should you invest $1,000 in ASML right now?

Before you buy stock in ASML, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ASML wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $845,679!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML and Nvidia. The Motley Fool has a disclosure policy.

ASML Stock Keeps Falling: Time to Buy the Potential Stock-Split Stock? was originally published by The Motley Fool

Leave a Comment